Table of Content

The calculations will be very close to reality, as long as your lender doesn't charge you fees for making prepayments. But, the amortization table probably won't match exactly what your lender provides. There are many ways to use equity to pay off your mortgage, but two of the most common approaches are second mortgages and home equity lines of credit . Second mortgages have the same payment each month and give you a lump sum at the start of the loan, which you could use to pay off some or all of your mortgage.

Change the "Enroll in Paperless Statements" toggle to on and read and agree to the "online statement and document delivery authorization" disclosure. Once enrolled, your statements will no longer be mailed to you in paper form. You may change your preferences at any time by following the above steps and clicking the toggle button again. Electronic statements are available online for your convenience and the safety of your account information. When you receive them electronically, you reduce the risk of identity theft, eliminate having to store them, and get immediate access to view, print or save statements/documents.

Please enter your city and state to find your ZIP Code

Homeowners can usually borrow up to 80% against the value of their home minus the amount that they owe on the mortgage. The approval process for HELOC is similar to when the borrower is getting their initial mortgage. Lenders will check their credit score, income, pay stubs, employment history, and debt to determine how much credit line to grant and at what interest rate. Amortization is paying off a debt over time in equal installments. Part of each payment goes toward the loan principal, and part goes toward interest. As the loan amortizes, the amount going toward principal starts out small, and gradually grows larger month by month.

Also known as a second mortgage, this type of loan turns your home’s equity into a lump sum of cash. How much principal and interest are paid in any particular payment. A cash-out refinance is a mortgage refinancing option that lets you convert home equity into cash. A home equity loan is a consumer loan allowing homeowners to borrow against the equity in their home. You can visit any Wells Fargo branch to make payments to your home equity account or to set up recurring payments.

Business payments

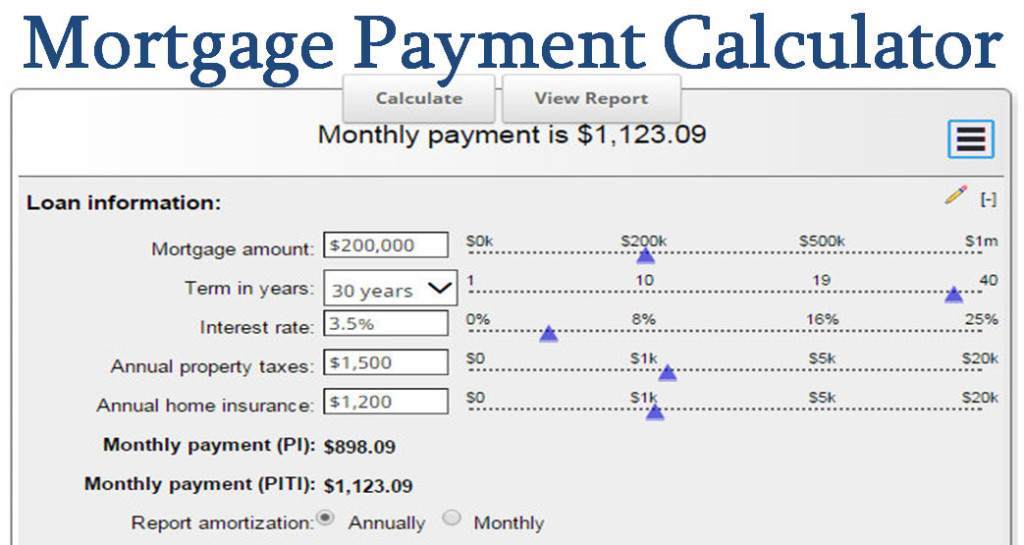

The terms are often used interchangeably, and almost any mortgage calculator can be used for a home equity loan. This calculator evaluates a fixed-rate loan, with optional extra payments (which you set up to simulate accelerated bi-weekly payments). If you need an adjustable rate mortgage calculator, you can try the ARM mortgage calculator. If you are looking for a home equity line of credit calculator, try our HELOC calculator. Your monthly mortgage payments are determined by a number of factors, including your principal loan amount, monthly interest rate and loan term. A higher interest rate, higher principal balance, and longer loan term can all contribute to a larger monthly payment.

For home equity loans and lines, only payment due date can be selected while setting up Auto-Pay. If payment due date falls within 3 business days, Auto-Pay will begin with your next payment due date. You can pay your bill through online or mobile banking, by phone, by mail or at a nearby branch, without having your statement with you.

Manage your account and pay online

The HomeEquity worksheet lets you calculate the amount of equity in your home after a number of years. Although it is limited to analyzing fix-rate mortgages, it can be very handy for analyzing your current state, and making useful predictions in case you want to sell your home later. Bankrate.com is an independent, advertising-supported publisher and comparison service. Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Bankrate.com does not include all companies or all available products.

During your 10-year draw period, you can borrow as little or as much as you need, up to your approved credit line. You have the option to choose a minimum monthly payment of 1% or 2% of your outstanding balance, though some may qualify to make interest-only monthly payments. The minimum monthly payment shown in your results reflects interest-only monthly payments. Amortization is the process of paying off a debt with a known repayment term in regular installments over time.

HELOCs are a revolving line of credit that you are free to withdraw from or repay as you see fit. Both of these loans carry much lower interest rates than credit cards or other unsecured loans, because they use your house as collateral. The main reason why homeowners take out home equity loans to pay down their mortgage is that they think doing so will result in lower monthly payments.

Unlike other home equity loan calculators, this one lets you include your 1st mortgage and your 2nd mortgage . It will work for interest-only mortgages , and if you enter a monthly payment larger than the normal amortized monthly payment, it assumes that the extra payment is going towards the principal. The HELOC calculator will calculate the monthly payments for both the draw period and the repayment period of a HELOC. During the draw period, the borrower has the option to make interest-only payments. After the draw period is over, borrowers are required to make principal plus interest payments which is the repayment period.

To be sure your payment is received on time, allow 7-10 business days before your due date. If you’re having trouble making payments on a KeyBank home equity loan or home equity line of credit because of the coronavirus pandemic, you can ask for deferral. For information on other assistance options, visit KeyBank Borrower Assistance. Federal law allows creditors and loan servicers to provide borrowers with electronic statements, but only with the consumer’s consent.

Repayment options may vary based on credit qualifications. Loans are subject to credit approval and program guidelines. Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice. Credit line may be reduced or additional extensions of credit limited if certain circumstances occur.

If the estimated monthly payment of your home equity loan or HELOC is higher than you’d like, use our tips to lower it. The interest rate is the rate at which the amount of money owed increases. It is typically expressed as an Annual Percentage Rate and incorporates any fees charged by the lender. Determine how much extra you would need to pay every month to repay the full mortgage in, say, 22 years instead of 30 years.

In an amortization schedule, you can see how much money you pay in principal and interest over time. Use this calculator to input the details of your loan and see how those payments break down over your loan term. Finally, homeowners would need to carefully evaluate the terms of the home equity loans that they are considering. By contrast, second mortgages follow a strict amortization schedule in which each payment includes both interest and principal. Technically, HELOCs offer a period of time, called a draw period, in which the borrower is free to pay only interest. However, at the end of the draw period, the HELOC converts to an amortization schedule, forcing the borrower to gradually pay back any principal that they borrowed.

Our rate table lists current home equity offers in your area, which you can use to find a local lender or compare against other loan options. From the select box you can choose between HELOCs and home equity loans of a 5, 10, 15, 20 or 30 year duration. There are benefits and drawbacks of getting HELOC versus other types of loans and credit cards.

Enter your loan amount, term and interest rate to estimate your monthly payment. Lastly, a home loan modification brings the home loan current for borrowers experiencing financial hardship. While a loan modification might allow you to become mortgage-free faster, and could reduce your interest burden as well, this option may negatively impact your credit. When you pay off your mortgage, the HELOC would be paid off at the same time.

No comments:

Post a Comment